November 28, 2022

Selling Property this Festive Season: The Tax Angle

December and January have always been prime months for selling residential property in South Africa, and if you are a “Festive Season Seller”, here are two really important tips for you.

- Plan your finances

Understand and plan for all the financial implications, not just the legal ones.Prepare a cash-flow forecast so that you know what you will receive and when, and what you will have to pay and when. Your forecast will tell you what funds you must have available at all stages of the sale and transfer process, and it will answer your bottom-line question – what will be left in your pocket at the end of it all? - Don’t forget your CGT liability

There are many expenses you should provide for (ask your lawyer to help you list them), but in this article we’ll only address one of them – the CGT (Capital Gains Tax) aspect.

This is vital – if you made a “capital gain” on the sale (more on how to calculate that below) you could be liable to pay CGT. If so, it could well be a substantial liability, and not planning for it will leave you in a world of pain because if you can’t pay your tax bill SARS will be after you with a big stick (SARS has extensive powers when it comes to debt collection).

There is a bit of good news: The advantages of owning your own family home, and the value of property generally as an investment channel, will for most people outweigh the pain of having to pay tax when you eventually sell. Plus, as we shall see below, paying CGT on a property sale is not nearly as painful as it would be to pay income tax on it. Indeed, if the capital gain on your primary residence is R2m or less, your CGT bill is nil!

How does CGT on a property sale work?

This is a complex topic, so what follows is of necessity a summary of general principles only – there is no substitute for specific professional advice here!

- What is Capital Gains Tax? CGT forms part of your income tax and is a tax on any “capital gain” you make on an asset, in this case a property. The capital gain is the difference between your base cost and the proceeds of your sale.

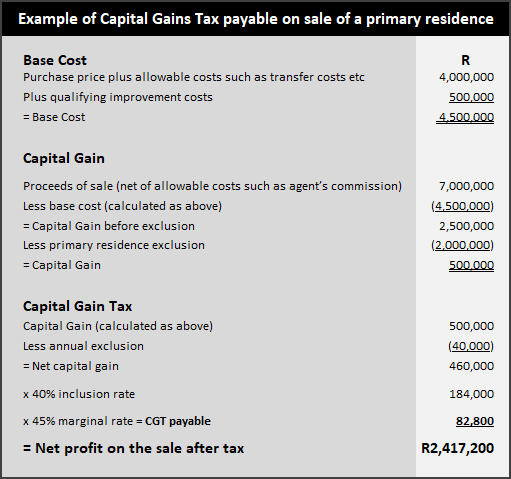

- What is “base cost”? This is what your property cost you to acquire (including transfer costs, transfer duty and the like) when you bought it. Note that CGT only kicked in on 1 October 2001, so if you bought the property before then it is the property’s value at that date that you will use. Qualifying improvement costs (extensions, additions and the like but excluding maintenance or repair costs) are also added to your base cost, so keep a separate note and proof of these as you incur them over the years. Our example calculation below assumes a homeowner who bought a number of years ago for R4m inclusive of transfer costs and duty, then spent a total of R500k on improvements (perhaps adding an extra room and a swimming pool).

- How do you calculate the “sale proceeds”? From the sale price you can deduct any costs of selling which are directly related to the sale, such as agent’s commission, advertising, legal costs and so on. In our example we assume net sale proceeds of R7m.

- How do you calculate the “capital gain”? This is the difference between the base cost and the proceeds of the sale (R2.5m in our example, before the primary residence exclusion).

- What can you deduct from the capital gain? If the property is in your personal name and is your “primary residence” (i.e., where you normally live) you can deduct a R2m exclusion from the capital gain. Note that if you used your house for business purposes or if you didn’t reside in it for the whole period of ownership, you need to take specific advice on how much (if any) of the exclusion is available to you. You can also deduct an “annual exclusion” of R40,000. In our example we assume the seller is entitled to both exclusions in full, resulting in a net capital gain of R460,000.

- How are you taxed on the net capital gain? The example below will help clarify this. Your capital gain is added to your annual income tax liability at the “inclusion rate” applicable to you. Individuals and special trusts have an inclusion rate of 40%, whereas other trusts and companies have an inclusion rate of 80%. You will then pay tax on that amount at your marginal tax rate (18% – 45% depending on your taxable income). In our example we assume an individual taxpayer paying tax at the highest marginal rate of 45%, the resulting tax liability of R82,800 amounting to just under 1.2% of the net sale proceeds. Our seller’s profit on the sale net of tax would then be R2,417,200.

So how much CGT will you actually pay?

For an individual your calculation is: Capital Gains Tax = Capital Gain x 40% inclusion rate x your marginal tax rate.

Have a look at the example below which assumes an individual home seller entitled to the full R2m primary residence exclusion and paying tax at the highest marginal tax rate of 45%. Then use your own figures and make your own calculation.

(Source: Adapted from SARS examples)

Disclaimer: The information provided herein should not be used or relied on as professional advice. No liability can be accepted for any errors or omissions nor for any loss or damage arising from reliance upon any information herein. Always contact your professional adviser for specific and detailed advice.

© LawDotNew

{kind=link}

November 28, 2022

Generational Wealth Planning – To Your Children and Beyond!

“Are we being good ancestors?” (Jonas Salk)

What do you plan to give your family this Festive Season? Now’s the time to think beyond the brightly wrapped gifts under the tree and get started on an estate plan which will leave your loved ones the lasting gift of financial freedom.

Estate planning involves a lot more than just executing a valid will, but let’s start off with a reminder that a will must always be your top priority.

Your will is the heart of your estate plan

You will have heard this many times before, but it bears repeating. Your will (“Last Will and Testament”) could well be the most important document you ever sign. Without executing a will, you forfeit your right (and duty) to decide how your assets will be distributed so as to ensure the future happiness and well-being of your loved ones. You lose your opportunity to choose an executor you can trust to wind up your estate professionally and efficiently. And no matter your age or state, it cannot wait – no one knows when the fateful day will dawn.

Most importantly, your will lies at the heart of your entire estate plan. It underpins and powers it. So, if you don’t yet have a will in place (or if your will needs updating) make your number one priority: “Book an appointment with my lawyer. Now.” Then ask your lawyer to draft your will to form the core of your overall estate plan.

What is an estate plan and why should you have one?

Your estate plan is your roadmap to creating wealth, to protecting it, and to transferring it to the next generation (or beyond). It is the only sure-fire way of ensuring your own comfortable retirement and of providing for the financial wellbeing of your loved ones after you are gone.

It incorporates your overall financial strategy, answering questions such as how you will save and invest, what investment options you will choose, how you will acquire assets, how you will provide for tax and other liabilities, how you will ensure effective succession planning in your business, how you will transfer your wealth to the next generation and so on.

Bring your family in early

It’s never easy contemplating one’s own mortality but in fairness to your loved ones make sure that as soon as they are old enough to participate, everyone is part of the process. Bring them in on everything you can and keep them in the loop when you are tracking progress or thinking of changing anything.

Questions to ask yourself

As the old adage has it “Failing to plan is planning to fail”. So plan. Start by asking yourself (and your family) these questions –

- What is our end goal?

- How much wealth do we need to build up?

- What is our target date for reaching that goal?

- How will we achieve it?

Now formulate your financial mission statement

Use your answers to those questions to formulate a “financial mission statement” and a detailed strategy to get there. As always with goal setting, break the big goals down into little ones, with target dates for achieving them and ways of tracking your progress.

Done and dusted! But wait, how will you actually transfer that wealth to the next generation (or beyond)?

Preserving your wealth for the next generation – and beyond

For many, it’s only realistic to plan one or two generations ahead. But whether your aim is to provide financial cover for just your spouse and children, or for your grandchildren as well, or (let’s aim high here!) for your great grandchildren and beyond, your estate plan should lay out a clear strategy for preserving your wealth down the generations.

Trusts are often recommended for generational wealth preservation and transfer, and whilst they have pitfalls and should only be considered with professional advice, they can certainly provide a powerful solution. In particular they could result in substantial estate duty savings for many generations down the line. Similarly, corporate structures (companies, company/trust combinations and the like) are often used for this purpose, particularly when trading businesses are involved. Donations during your lifetime may be suggested but beware the tax implications. Living annuities enable you to nominate beneficiaries to receive the benefits (with a tax incentive for them to leave at least part of the funds invested). There may be other niche solutions to suit your particular needs.

The bottom line

There are many complex decisions to be made and there is no “one size fits all” solution. Every family’s situation and needs will be unique. Every class of asset and every wealth-transfer vehicle carries with it particular requirements, benefits, risks and cost and tax considerations.

Professional advice specific to you and your family is essential!

Disclaimer: The information provided herein should not be used or relied on as professional advice. No liability can be accepted for any errors or omissions nor for any loss or damage arising from reliance upon any information herein. Always contact your professional adviser for specific and detailed advice.

© LawDotNews

{kind=link}

November 28, 2022

A “Running Down” Damages Claim – Elite Athlete v Happy Snapper

“This is a running down case: literally” (Extract from judgment below)

The scene is Cape Town’s iconic Sea Point Promenade. An elite runner participating in a race knocks down a pedestrian out for a Sunday walk, causing serious injuries. The pedestrian sues both the runner and the race organiser for damages of R718,000.

The outcome is another reminder to us all to be aware of our surroundings at all times – a moment’s inattention can change everything in a split second. As the facts here illustrate…

The race-day collision and the R718,000 claim

- Although the Court heard conflicting evidence as to detail, the setting for this unfortunate collision was common cause. A popular public space on a Sunday, replete with not only the normal pedestrians, cyclists, dog walkers and kite-flyers, but on this particular day also thousands of participants in a “Ladies Race”, ranging from athletes competing in an “elite race” to costumed “Fun Walk” entrants.

- Going for a Sunday stroll with a friend and “in the wrong place at the wrong time” whilst blissfully unaware of the misfortune about to be visited upon her for her act of goodwill, the claimant happily consented to a request from a group of “Fun Walk” participants to take a “happy snap” of them.

- Picture taken, she moved across the sidewalk to hand the camera back to its owner and a participant in the “elite race” ran straight into her, then ran off to finish her race.

- Suggestions that the runner (approaching it seems at about 20 kph) shouted a warning to the effect of “get out of my way” and forcefully pushed the claimant aside were in dispute, but what was clear was that she was knocked to the ground and sustained a hip injury which resulted in an ambulance trip to hospital and hip replacement surgery.

- The claimant sued both the runner and the race organiser for R718,000 in damages. The Court’s findings hold lessons for us all.

The race organiser off the hook

On the evidence, the race organiser and the race Marshall in the vicinity of the collision were cleared of any negligence.

The runner’s negligence

The runner, found the Court, was in a public space and should have been alive to the possibility of encountering other sidewalk users at close quarters. She had a duty to keep a proper look out and should have taken into account “the nonchalance and lack of interest of ordinary pedestrians who were out and about enjoying the fresh air rather than watching an athletics race. Ordinary human experience tells one that such persons might behave irrationally and get in the way, as it were.” (Emphasis added).

The runner was negligent in focussing only on the ground immediately ahead of her, “running as if in a bubble, oblivious to what was happening around her and intent only on achieving her goal of winning the race.” She could have avoided the collision with little effort and without seriously affecting her chances in the race.

The pedestrian’s 70% contributory negligence

However, in all the circumstances the Court held that the claimant (actually the executor of her estate as she had later died from unrelated causes) was only entitled to 30% of whatever damages could be proved.

She had been, said the Court, considerably more negligent than the runner. She had to be aware of the race, she knew runners were “whizzing” past her, and she had been warned of runners coming through.

The old ironic saying “no good deed goes unpunished” springs to mind, but the hard fact (in life as in law) is that we are often the architects of our own misfortune.

Be aware of your surroundings at all times!

It’s a hard lesson, but the law holds us to certain standards, and one of those is to keep a proper look out, particularly when in a public space. A moment’s inattention, and in a split second your life could change forever, with physical injuries compounded by the risk of damages claims and counterclaims of contributory negligence.

Take legal advice immediately if you are unlucky enough to be involved in an incident causing injury or other loss!

Disclaimer: The information provided herein should not be used or relied on as professional advice. No liability can be accepted for any errors or omissions nor for any loss or damage arising from reliance upon any information herein. Always contact your professional adviser for specific and detailed advice.

© LawDotNews

{kind=link}

November 28, 2022

Website of the Month: Don’t Stress this Silly Season!

“You can tell a lot about a person by the way they handle three things: a rainy day, lost luggage and tangled Christmas tree lights.” (Maya Angelou)

December holidays are a time for winding down, recharging your batteries and sharing some quality family time. But it can also be stressful. There’s a reason we often talk about the “Silly Season”.

Don’t let the pressure get to you! Relax, take a deep breath, and read “10 tips to reduce festive season stress” on the Lionesses of Africa website.

Whatever else you do, enjoy your break!

Disclaimer: The information provided herein should not be used or relied on as professional advice. No liability can be accepted for any errors or omissions nor for any loss or damage arising from reliance upon any information herein. Always contact your professional adviser for specific and detailed advice.

© LawDotNews

{kind=link}

November 15, 2022

KVV | A Note from our Director

I recently read that some parts of the world celebrated something called “international kindness day” on 13 November 2022. My first thought was probably the same as the thought that many of you might have at first and it went something like “Ahhhhh why do we need a special made-up day for every little thing”.

However, it would be dishonest of me to say that I did not find myself continuously reconsidering the idea throughout the next couple of days. The idea of a day dedicated to random acts of kindness seemed to inextricably draw me in the more I thought of it. Kindness, in its truest form, is doing something helpful or thoughtful for someone (that someone often being weaker or more vulnerable than you), with no hope of reward or gain and purely for the purpose of, well, kindness.

The news nowadays is completely devoid of stories relating to kindness and we often hear people lamenting the cruelty of the world and the life we find ourselves in. But, oh my, allow yourself to dream with me and consider for a moment a world where people treat all other people with kindness. Imagine a world where motorists approach a “loadshedded” intersection with smiles, leeway and kindness. Imagine a world where a random stranger pays for your coffee at Starbucks one morning, unaware that you are exhausted from staying up all night with your sick toddler.

I know the idea seems foreign, I know that it goes against the grain sometimes. But many of us work with people on a daily basis. We speak to hundreds of people on a weekly basis whether it be the person in front of you in a line, a colleague or client or simply just some random person in a shop somewhere. Imagine the impact that one act of kindness per person per day could achieve.

Bob Kerrey once said that unexpected kindness is the most powerful, least costly and most underrated agent of human change. I want to challenge you the next couple of months to be the change that you want to see in people. I want to challenge you to go out there and change the world with kindness. I want to challenge you to realise that the power to change the world might literally reside in your smile.

Regards

Ianthe Biggs | Associate

{kind=link}

November 15, 2022

Bond Clauses: Beware the Deadlines!

“I love deadlines. I love the whooshing noise they make as they go by.” (Douglas Adams)Here’s yet another reminder from our courts on the danger of not complying strictly with every provision in a property sale agreement. Don’t be like Douglas Adams and listen to the deadlines go whooshing by – missing a property sale deadline is a mistake, probably an expensive one. The deadline set by every bond clause is no exception…

Sale’s a dead duck. Who gets the R600,000 deposit?

-

- A property sale agreement contained a standard “suspensive condition” in the form of a bond clause making the sale conditional upon the buyer obtaining R1.5m in bond finance by a specified date. The buyer could waive the benefit of this clause, and if it wasn’t fulfilled or waived by the deadline date the sale would become null and void – in which event the deposit, with interest, was to be repaid to the buyer within 5 business days.

-

- The buyer paid the R600,000 deposit to the estate agent, but had difficulty in raising finance and (before the deadline expired) asked for more time to get the necessary bond approval. Both parties assumed that an extension of the deadline had been validly granted, but in fact there was never any compliance with the requirement in the bond clause that any extension be by “written agreement”. In other words, the sale had lapsed, but neither the seller nor the buyer realised that – they both thought they still had an agreement in place.

-

- Two months later, thinking that the sale was still alive and well, the buyer signed a waiver giving up the benefit of the bond clause and stating that the agreement was no longer subject to the suspensive condition.

-

- Another two months down the line the buyer told the seller he was no longer proceeding with the purchase (his wife had in fact bought another property in the interim). The seller took that as a repudiation of the contract and cancelled the sale.

-

- The buyer demanded his deposit back. The seller wanted it forfeited to him. Off to the High Court they went.

The law, and the result

-

- The general rule in our law is that no agreement comes into existence unless and until all suspensive conditions are fulfilled. So the seller has no claim against the buyer unless either the sale agreement provides for such a claim (unlikely) or “where the party has designedly prevented the fulfilment of the condition.”

-

- That, in lawyer-speak, is the legal principle of “fictional fulfillment of a suspensive condition”. In lay terms – the law protects the seller and doesn’t allow the buyer to escape from the sale by deliberately ensuring that he doesn’t get a bond.

-

- The seller argued that that was exactly what the buyer in this case had done; that he had breached the agreement and had deliberately frustrated the fulfilment of the bond clause.

-

- On the facts however, the Court held that both seller and buyer had remained committed to the sale, blissfully unaware that in law the sale agreement was already a dead duck. The buyer only decided to get out of the agreement after it had already lapsed.

-

- The buyer gets his deposit back with interest, and the seller is left with an unsold property and a large legal bill.

Buyers – your risk

As the Court put it, what saved the buyer in this case was a lack of evidence that the buyer had – by commission or omission – prevented the necessary finance from being granted. In other words, you risk being sued (which will put your deposit at risk) if you don’t make a genuine effort to get the necessary bond finance by the due date.Sellers – keep an eye on the bond clause deadline

The seller on the other hand is left to lick his wounds after all the delay, cost and effort this dispute has caused him. He could have avoided all that pain by keeping an eye on the due date and ensuring that the deadline extension was agreed to in writing before it expired. As the Court pointed out “The contract was readily available to all involved and the requirements of clause 6.3 pertaining to an extension were available for all to read. A simple investigation would have revealed what was required.” (Emphasis added). Disclaimer: The information provided herein should not be used or relied on as professional advice. No liability can be accepted for any errors or omissions nor for any loss or damage arising from reliance upon any information herein. Always contact your professional adviser for specific and detailed advice.© LawDotNews

{kind=link}

November 15, 2022

Building in Security Estates: The ‘Persuasive Sting’ of Penalty Levies

“… had the respondent imposed more moderate penalties, it would likely not have had the desired effect, or put differently, the same persuasive sting for individuals of substantial means.” (Extract from judgment below)Buying “plot and plan” in a residential complex allows you the freedom to build your own dream house in a secure environment, quite apart from providing what is likely to be sound long-term investment. Just make sure that you will actually be ready to build within the time frame required by the HOA (homeowners’ association). If you don’t, you risk having to transfer the plot back to the developer (a costly exercise), or you could be lumbered with penalty levies many times higher than normal levies.

You can ask a court to reduce the penalty, but…

Our law gives us general protection from excessive “out of proportion” penalties by means of the Conventional Penalties Act, which in the section headed “Reduction of excessive penalty” provides that – “If upon the hearing of a claim for a penalty, it appears to the court that such penalty is out of proportion to the prejudice suffered by the creditor by reason of the act or omission in respect of which the penalty was stipulated, the court may reduce the penalty to such extent as it may consider equitable in the circumstances: Provided that in determining the extent of such prejudice the court shall take into consideration not only the creditor’s proprietary interest, but every other rightful interest which may be affected by the act or omission in question.” However, as a recent High Court decision illustrates, you will have your work cut out for you if you want the court to exercise that discretion in regard to penalty levies.The ‘persuasive sting’ of 5x normal penalties

-

- The HOA of a “luxury/ultra-luxury” residential estate required in its constitution that –

- Each owner must start construction within one year of transfer,

- Should construction not commence timeously the developer had the option to require re-transfer of the erf to it,

-

- If the developer did not exercise this option, the HOA could “impose whatever penalties it deems appropriate in its sole discretion” on the owner.

- The HOA of a “luxury/ultra-luxury” residential estate required in its constitution that –

-

- When several erf owners failed to build within the one-year deadline, the HOA passed resolutions imposing penalty levies on them until they started construction.

-

- These levies started off at 2x the normal levies, and over an eight-year period were increased in stages to 5x the normal.

-

- The HOA sued the defaulting owners in the Regional Court to recover these levies, winning both in that Court and on appeal to the High Court.

-

- It was, held the High Court, up to the owners challenging the amount of the penalty to prove –

- What prejudice the HOA suffered,

- That the penalty was disproportionate to that prejudice, and

-

- The extent to which the penalty should be reduced.

- It was, held the High Court, up to the owners challenging the amount of the penalty to prove –

-

- In addition to the actual monetary prejudice (damages) suffered by the HOA, it was said the Court necessary to consider the HOA’s other “rightful interests” that might be affected by the failure to build, such as problems with security, nuisance, aesthetics, damage, and value loss caused by extended building activities. In this case, one of the additional reasons for the penalty provision was to discourage speculation in the erven by buyers intending to re-sell the plots for profit rather than build and live in the estate.

-

- There was prejudice to the HOA even though the penalty provision was intended to create a deterrent rather than compensation for default – the prejudice was to the HOA’s “right to enforce concerted action for the common good, and to its interest in obtaining concerted action”.

-

- Whether the penalty was “out of proportion” to the prejudice could be assessed in three ways:

-

- By looking at comparable situations where the desired result was achieved (the Court compared another similar matter in which a 10x normal penalty was reduced by the Court to 8x normal, much more than the 5x imposed here),

-

- By looking at the size of this penalty and the penalties in general in relation to the income and expenditure of the HOA, and

-

- “By exercising one’s sense of fairness and justice.”

-

- Whether the penalty was “out of proportion” to the prejudice could be assessed in three ways:

-

- The HOA had been fair and reasonable in phasing in the increases over an eight-year period.

-

- Imposing more “moderate” penalties “would likely not have had the desired effect, or put differently, the same persuasive sting for individuals of substantial means.”

© LawDotNews

{kind=link}

November 15, 2022

If the Municipality Rejects Your Building Plans, Consider PAJA

“The Constitution guarantees that administrative action will be reasonable, lawful and procedurally fair. It also makes sure that you have the right to request reasons for administrative action that negatively affects you.” (Department of Justice and Constitutional Development)Bureaucratic decisions can and do have far-reaching consequences for us, both financially and in our personal lives. It’s good to know therefore that whenever your rights are affected by any such decision, you have access to the protections set out in PAJA (the Promotion of Administrative Justice Act). In a nutshell, PAJA provides that “administrative decisions” by government departments, parastatals and the like must be fair, lawful and reasonable. Decision makers must follow fair procedures, allow you to have your say before deciding, and give you written reasons for their decisions when asked. If a decision goes against you, your first step should be to use any internal appeal procedures. Ultimately you can go to court, although often a lawyer’s letter or two will solve the problem without the need for litigation. A recent High Court decision illustrates one way in which PAJA can help you if all else fails –

A service station’s building plans rejected

-

- A service station submitted to its local authority building plans for a proposed refurbishment.

-

- After a series of meetings with the municipality and alterations to the plans as various issues were raised and resolved, the service station owners thought they were home and dry. But in the end the plans were not accepted on the basis that the application was for an extension of the service station which could not be approved in terms of the local Town Planning Scheme.

-

- The High Court however found that factually there was no “extension” involved and that the municipality had therefore made an “error in law”.

-

- That opened the door for the Court to review the municipality’s decision, which it duly set aside. In referring the decision back to the municipality for reconsideration, the Court directed it to make a decision within 21 days, and without regarding the proposed refurbishment as being an extension of the building.

© LawDotNews

{kind=link}

November 15, 2022

Why You Should Sign a Power of Attorney Before You Emigrate or Travel

If you are emigrating, or perhaps just going overseas for an extended holiday or work contract, you may well leave behind some form of “unfinished business”. Perhaps you own a property, other assets or bank accounts needing attention, or have outstanding tax/business/financial affairs, or contracts to be signed, cars to be licenced, or something else unresolved that requires your future agreement or signature. Even if you can’t think of anything specific, consider executing (before you leave of course) an appropriate power of attorney in favour of someone you trust to act for you.What is a power of attorney?

A Power of Attorney (“POA”) a document you sign authorising someone else to manage your affairs on your behalf as your agent. You can grant it for a specific purpose as a “Special Power of Attorney” or it can be a widely worded “General Power of Attorney”. In theory you can grant power of attorney orally, but in practice no one will (or should) act on that. You must be at least 18 years old to execute a POA, and it remains valid only for so long as you have “legal capacity”. You can terminate the POA at any time.Why is a power of attorney important?

You can in a pinch execute and sign contracts, legal forms and the like whilst in a foreign country, but it can be a real mission. Depending on the circumstances, you may need to find (and pay) a notary public or embassy/consular official to authenticate documents, your signature, copies of papers etc. If it’s an embassy or consulate you need, you could find yourself travelling to another city, perhaps even another country. And if everything isn’t done exactly right the first time (a particular risk if you are dealing with someone not fully versed in South African law and procedure), you could find yourself repeating the process – perhaps even more than once in a sort of “Ground Hog Day” scenario. All avoidable if you leave behind in South Africa a valid and correctly structured POA.How should you structure it?

The structure you will need depends on what affairs you need dealt with and why. It can be difficult to decide whether a POA is appropriate for a particular purpose, and if so how wide or how restricted you should make the powers you are granting to your agent. It can also be a challenge to find the correct wording to satisfy the requirements of whichever authority or other party is involved – for instance, specific forms are required by the Deeds Office, SARS, and banks. You might also need to leave behind more than one POA, each structured for a particular purpose. Similarly, you may be uncertain as to who to appoint as your agent, who is best qualified for each purpose, even perhaps who can you trust to act professionally and honestly. There is no prescribed form and no list of required formalities for a valid POA but there are many possible permutations and legal risks involved, so the only way to ensure that it is valid and fit-for-purpose is to seek professional assistance specific to your circumstances. Disclaimer: The information provided herein should not be used or relied on as professional advice. No liability can be accepted for any errors or omissions nor for any loss or damage arising from reliance upon any information herein. Always contact your professional adviser for specific and detailed advice.© LawDotNews

{kind=link}

November 15, 2022

It’s Wedding Season – Three Questions to Ask Before You Marry

“Marriage is a matter of more worth / Than to be dealt in by attorneyship” (Shakespeare)Wedding Season is well and truly upon us, and if you (or anyone near and dear to you) is busy planning for marriage (note that we are talking “civil marriage” here, “customary marriages” and “civil unions” are beyond the scope of this article), you will have a long “To Do” List to work through. Venue, invites, catering, flowers, service, this, that, the other. The list goes on, and on… But no matter how long or complicated your Wedding Plan may get, make sure that “Get All the Boring Legal Bits Sorted” is high on your priority list. Yes, this is the not-fun part of all this, and getting to grips with all the legal niceties is a chore. But whilst we can all agree with Shakespeare’s observation that “Marriage is a matter of more worth / Than to be dealt in by attorneyship”, understanding and managing the legal consequences of marriage remains absolutely vital. So, where to start? Ask your lawyer three questions –

1. “Do we need an ANC?”

Whether you need an ANC (antenuptial contract), and if so, what should be in it, will depend in part on which “marital regime” you choose. This is a critical decision. Which regime you choose now (and you must choose before you marry) will affect you and your family long after the ink dries on your marriage certificate. It will affect all of you throughout your marriage, and it will affect everyone when your marriage eventually comes to an end (whether by divorce or death – both grim prospects, but realities that must be faced). Our law presents you with three alternatives, and professional assistance is essential here because your choice involves a complex mix of individual preference, circumstance, and personal and financial status –- Marriage in community of property: All of your assets and liabilities are merged into one “joint estate” in which each of you has an undivided half share. On divorce or death the joint estate (including any profit or loss) is split equally between you, regardless of what each of you brought into the marriage or contributed to it thereafter. This is the “default” regime – so you will automatically be married in community of property if you don’t specify otherwise in an ANC executed before you marry. This regime will suit some couples, but most will be advised to rather choose one of the other options (b or c below).

- Marriage out of community of property without the accrual system: Your own assets and liabilities, both what you bring in and what you acquire during the marriage, remain exclusively yours to do with as you wish. Note here that the “accrual system” (see option c below) will apply to you unless your ANC specifically excludes it.

- Marriage out of community of property with the accrual system: As with the previous option, your own assets and liabilities remain solely yours. On divorce or death you share equally in the “accrual” (growth) of your assets (with a few exceptions) during the marriage.

2. “Are our wills in order?”

Marriage is one of those life events that focuses the mind on how important it is to have valid wills (or perhaps one “joint will”) in place. Existing wills need immediate review. Of course, your will (“Last Will and Testament”) is only the first step in a full estate planning exercise, but it is the foundational step, so prioritise it. Don’t be tempted to procrastinate on this one – as the old saying has it “Death Knocks at All Doors”, and often it knocks without warning. There’s no other way to ensure that your loved ones will be fully protected and catered for after you are gone.3. “Can we choose new surnames?”

As a man, you can only change your surname by application to DHA (the Department of Home Affairs) but as a woman you can automatically –- Take your husband’s surname, or

- Revert to or retain your maiden surname or any other prior surname, or

- Join your surname with your husband’s as a double-barreled surname.

© LawDotNews

{kind=link}